Allstate raised rates again in 2Q, says it’s been responding to frequency, severity

By onBusiness Practices | Insurance | Market Trends

Allstate told investors Thursday that it has been taking “aggressive actions” to manage rising costs of auto claim frequency and severity — including another quarter of premium rate increases.

Let’s hope the nation’s No. 3 auto insurer and its Top 10 peers prove as understanding when auto body shops apply the same logic and attempt to charge more per hour and charge at all for various procedures.

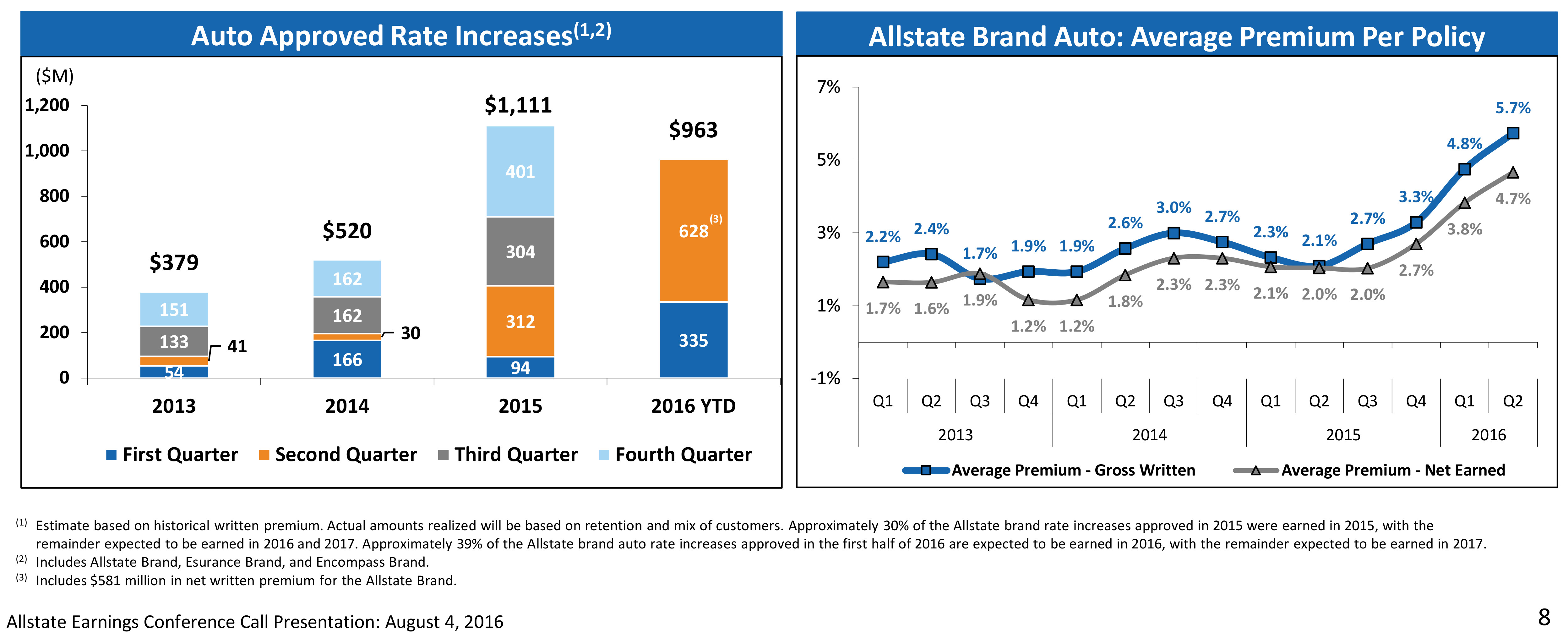

Allstate reported state regulators between April and June cleared it to charge a combined $628 million worth premium increases nationwide. To date, regulators have approved nearly a billion dollars more in rates in the first half of the year: $963 million.

Allstate doesn’t get to collect the money immediately, as it won’t charge customers the additional amount until it’s time to renew a policy. (For example, six months from now.) Allstate estimates that its brand of auto insurance (which doesn’t count Esurance or Encompass) ultimately will produce $581 million in net premium — what it actually banks.

Overall, Allstate reported that its average premium charged per policy was 5.7 percent higher in the second quarter of 2016 than in the prior year. Its actual banked premium revenue was 4.7 percent higher than in Q2 of 2015, indicating the same lag described above and other factor. (Someone switches carriers before their renewal date, for example).

So if Allstate adjustors give you grief for your bill, just point out that their company already knew more expensive cars and higher demand for repairs existed, and they’re charging more too. In doing so, they’ve also more than covered such differences.

“While auto policies declined, net written premium increased by 3.9 percent, which was essentially offset the impact of continued increases in frequency and severity,” CEO Tom Wilson told analysts, an apparent reference to the overall amount of money collected.

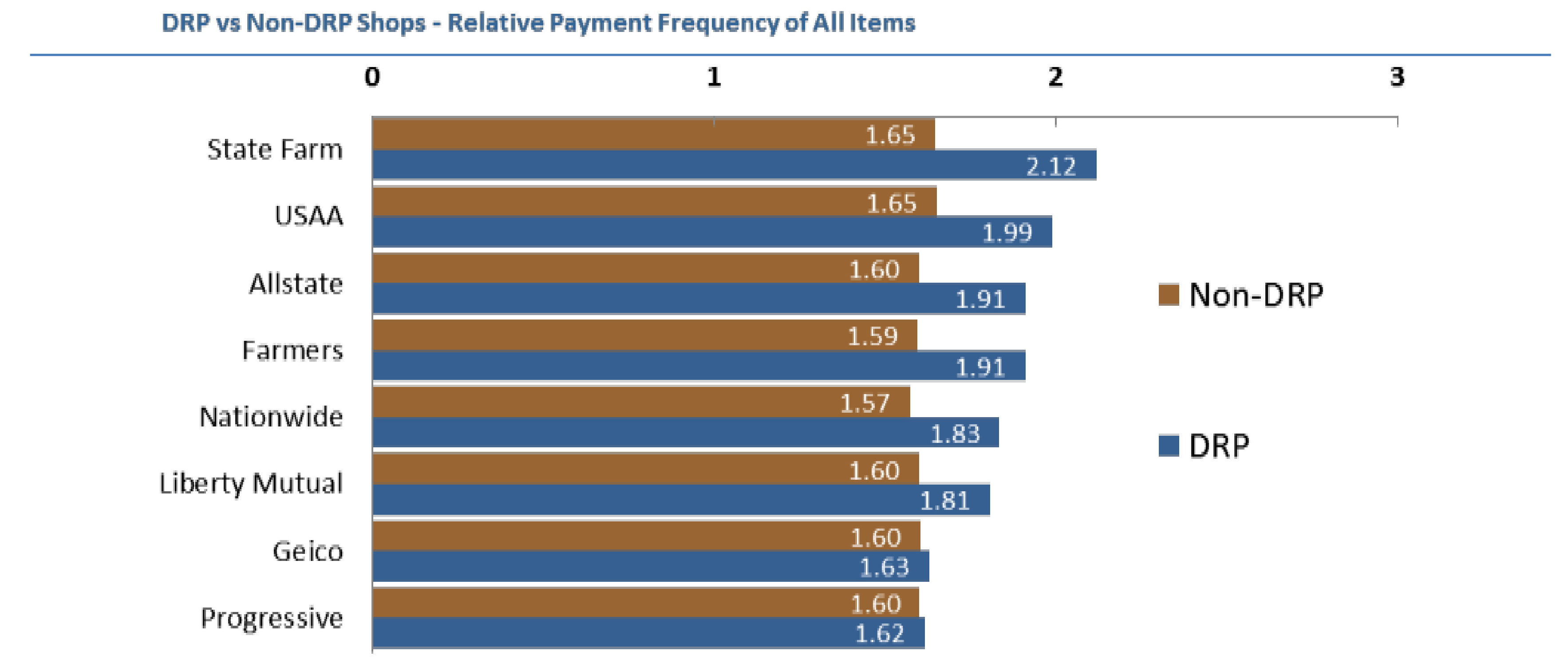

Collision repairers surveyed for the recent body labor “Who Pays for What?” study by Collision Advice and CRASH Network reported that Allstate and its other Top 8 insurance competitors all paid direct repair programs and non-DRP shops at least “some of the time.” (1 on a 0-3 scale.) However, only State Farm and USAA were reported to pay “most of the time.” (A 2 on that 0-3 scale.)

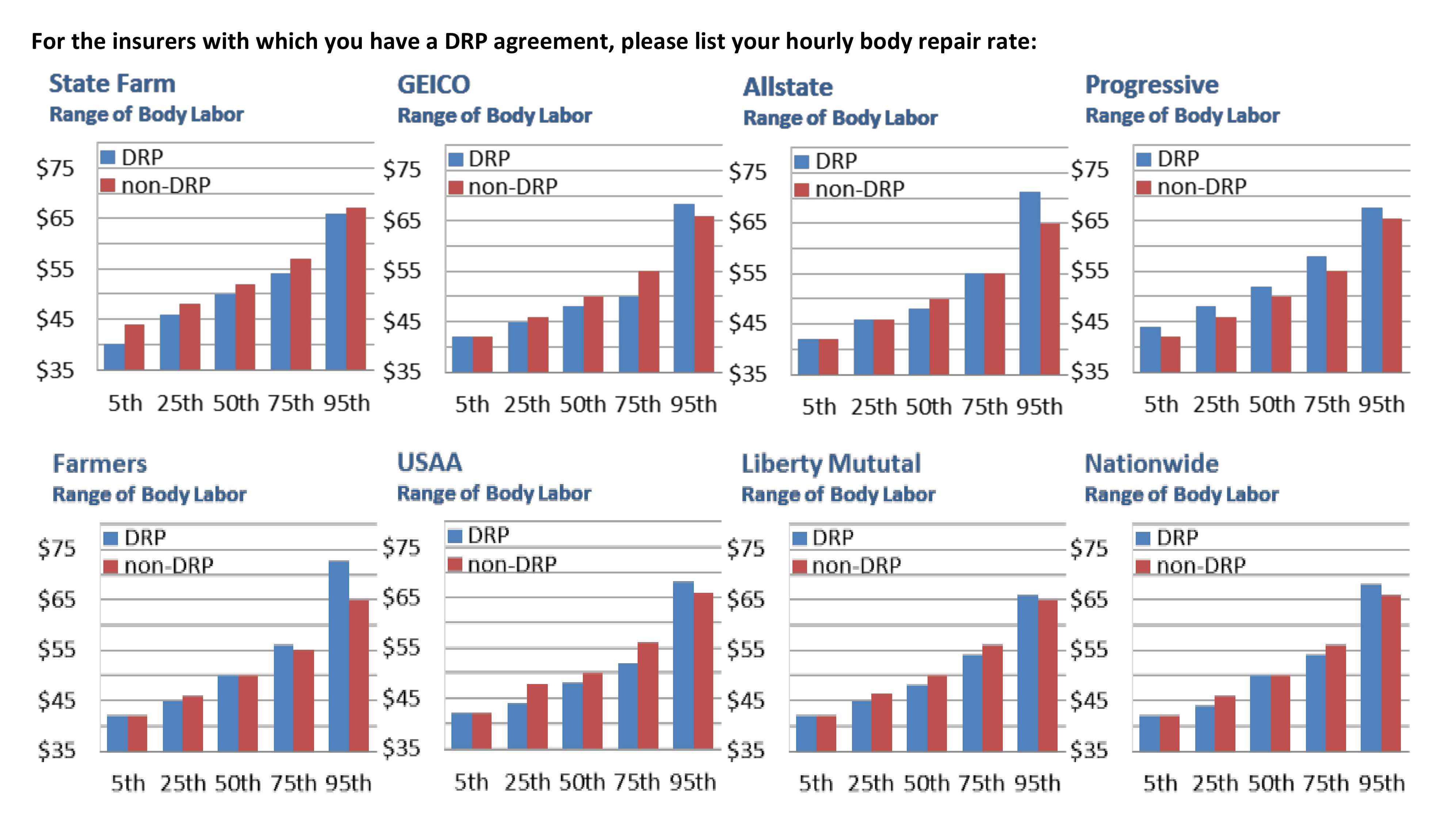

Here’s how Allstate and the other Top 8 insurers shook out in the survey in terms of body labor rates approved for DRP and non-DRP shops.

In terms of posted rates, the 50th percentile of repairers charged $54, with the 25th and 75th percentile charging $48 and $60, respectively.

A copy of the body repair “Who Pays for What?” survey can be obtained here.

Auto insurance nationwide rose 6.5 percent in June 2016 over June 2015 without seasonal adjustment, while auto body work has risen only 2.4 percent in that time. Both are ahead of inflation as measured by the Consumer Price Index, which was simply 1 percent.

“Given ongoing auto loss pressure, we continue to seek approval for higher auto prices,” incoming Encompass President Patrick Macellaro told analysts.

Besides seeking more than $1.1 billion in premium increases in 2015, preceded by hundreds of millions more requested in 2013 and 2014, Allstate also last year dialed back expenses, tightened underwriting and sought “excellence” on claims. The call with analysts Thursday indicated that reducing expenses and upping rates contributed the most to sustain Allstate’s financial results.

“Our early recognition of increased frequency and severity along with the aggressive actions we continue to take have enabled us to keep auto margins stable despite the continued challenging auto loss cost environment,” said Macellaro, who was on his last call as the vice president of investor relations.

“If we’d not moved early,” he said later, “our auto returns would be significantly lower and we’d be playing catch-up until well after the loss pressure we and others are experiencing subsides.”

Expense reduction efforts included lower compensation incentives, fewer dollars spent on professional services, and cutting marketing dollars. The company also courted fewer new agents, saving the money it would have spent getting those representatives up and running.

However, the company has launched one new campaign, and “we’re comfortable doing more advertising,” Wilson said. He told analysts to think of it more as marketing, as the company has opted to focus less on TV and more on digital ads, reflecting Americans’ habits.

More information:

Allstate second-quarter 2016 earnings webcast

Allstate, Aug. 4, 2016

Allstate second-quarter 2016 presentation to investors

Allstate, August 2016

Allstate, August 2016

“Allstate Net Income Impacted By Catastrophes”

Allstate, Aug. 3, 2016

“Who Pays for What?” 2016 body survey results

Collision Advice and CRASH Network

Images:

An Allstate insurance company sign is seen outside one of its stores Jan. 17, 2008. (Joe Raedle/Getty Images News/Thinkstock file)

Allstate offered this premium data to investors in its second-quarter 2016 presentation. (Provided by Allstate)

Collision repairers surveyed for the recent body labor “Who Pays for What?” study by Collision Advice and CRASH Network reported that Allstate and its other Top 8 insurance competitors all paid direct repair programs and non-DRP shops at least “some of the time.” (1 on a 0-3 scale.) However, only State Farm and USAA were reported to pay “most of the time.” (A 2 on that 0-3 scale.) (Provided by Collision Advice and CRASH Network)

Recent body repair labor rate data from a 2016 “Who Pays for What?” survey. (Provided by Collision Advice and CRASH Network)