Mitchell: Most claims under $2,500; check your shop data by studying $500-increment distribution

By onBusiness Practices | Education | Insurance | Market Trends | Repair Operations

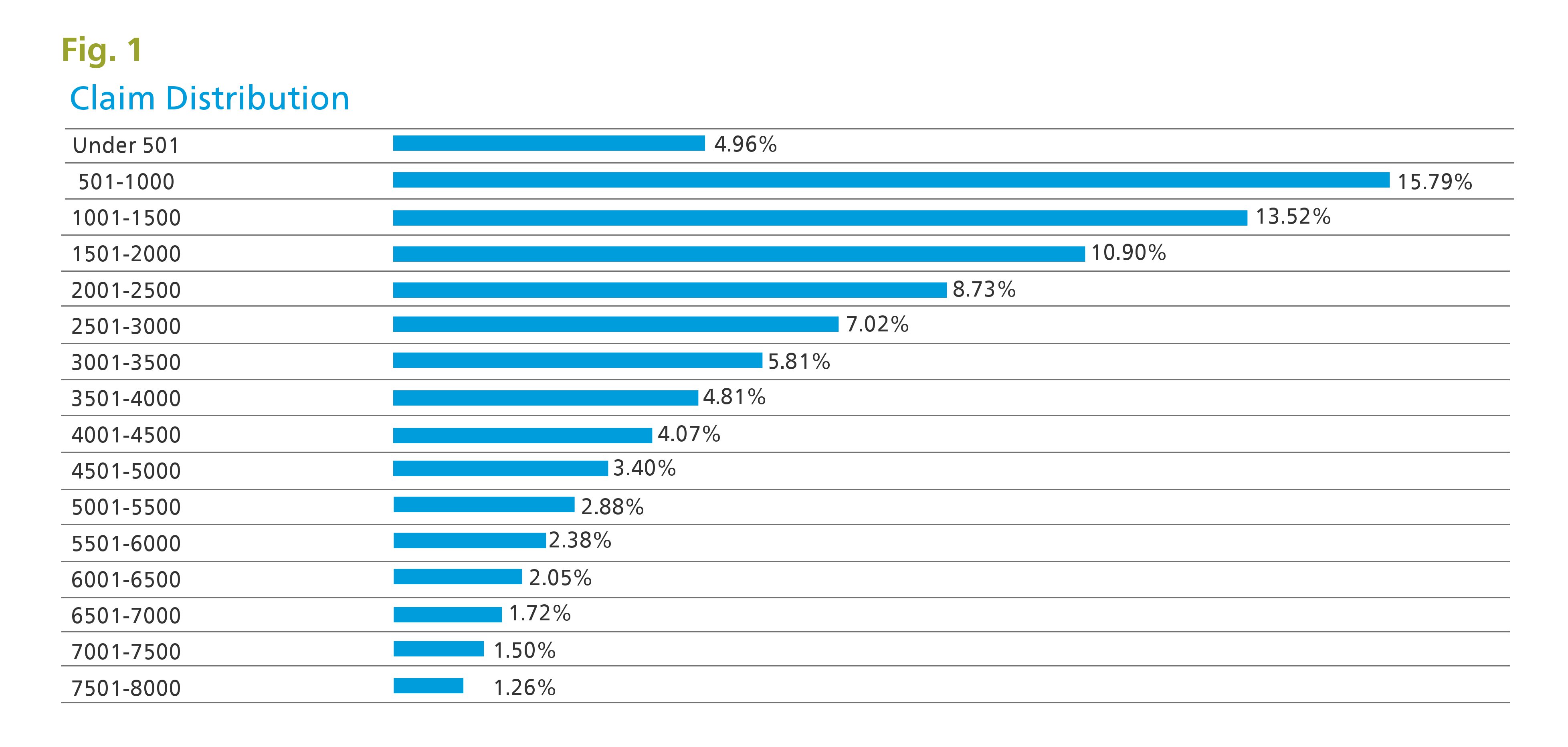

The majority of claims fall below $2,500 in gross severity, showing the need for insurers and repairers to truly know that type of damage inside and out, according to a new Mitchell article.

Mitchell’s latest Industry Trends Report data feature also provides a useful exercise for repairers: Break down one’s claims data into $500 increments and see what you find.

“Whether you operate a repair shop, write estimates for an insurance company or are an independent appraiser, showing how claims volume falls within $500 increments can provide key insight into how your business measures against the industry, or how your shop compares against other shops,” Mitchell industry relations Vice President Greg Horn wrote in the May quarterly report.

It’s unclear which dates the data span or if any sort of control was done for direct repair program shops’ cost concessions, which would skew the statistics downward.

The 53.90 percent of claims below $2,501 should tell shops they’ll be fixing more panels and bumpers, Horn wrote, and “repair decisions and accuracy are extremely important.” On a webinar Thursday about the data, he urged those involved in such cosmetic repairs to “bring your A game.”

“Lower cost claims yield more repairable bumpers, and repairs can be done faster than replacements,” Horn wrote.

“As I have noted in earlier articles, bumpers are present in 72% of repairable claims. The repairability of bumper covers in claims less than $2,500 is even greater than on high-cost/higher-damage claims. Claims under $2,500 will have more lightly-damaged bumper covers that can be repaired. Based on that, are the appraisers who are seeing claims under $2,500 at the leading edge of bumper repair education? They should be, as bumper repair education (and fixing more covers) can lead to greater efficiency for a shop – and lower claims costs for insurers.”

Of course, 46.10 percent of Mitchell’s analyzed claims were above $2,500, and Horn cautioned that just because a shop or appraiser’s individual $500-increment claims data runs higher doesn’t mean they were inefficient or failing to properly control costs.

“Another important aspect of the distribution involves looking at regions or offices of insurance companies, as well as the location of the individual appraiser over time,” Horn wrote. “Some direct repair shops and appraisers (both staff and IA’s) are unfairly penalized because the distribution of claims severity leans more towards pricier claims. Their production is lower, their supplement rate is above average, and the average severity is higher. This is not because the appraiser is less accurate, but because the appraiser has written appraisals on more heavily-damaged vehicles.”

And of course, there’s no way to force drivers crashing in your market area to produce damage that hews to the mean for a particular time period (For example, a DRP assessing member shops’ severity for a year, quarter or month.) or stop OEMs from advancing gadget and body technology and producing vehicles which are costlier to repair.

Horn in his report and in a webinar Thursday questioned the value of insurers paying $200 a pop for an appraiser to manage a claim for the slightly less than 5 percent of claims that fell $500 or lower. He wrote that those $500-and-under claims averaged a single part being replaced and a mean cost of $116.

On average, those claims have just over one part replaced, at an average cost of $116.

“Is that financially the most responsible way to inspect that vehicle?” he wondered Thursday. On the other hand, he said, there could be a customer service rationale for continuing to staff all claims with adjustors.

Finally, analyzing the distribution in $500 increments can be extremely useful for scheduling purposes, according to Horn. Similar advice can be found in this CIECAst video featuring Mike Anderson of Collision Advice and industry consultant Frank LaViola.

More information:

“Mitchell Issues Second Quarter 2016 Industry Trends Report”

Mitchell, May 9-10, 2016

Mitchell 2Q Industry Trends Report

Mitchell, May 9-10, 2016

Mitchell “Industry Trends Live” webinar

Mitchell, May 16, 2016

Images:

A swiped bumper. (JohnnyH5/iStock/Thinkstock)

The majority of claims fall below $2,500 in gross severity, showing the need for insurers and repairers to truly know that type of damage inside and out, according to a May 2016 Mitchell article. (Provided by Mitchell)