Mitchell guest column: OEM-aftermarket price spread dropping — particularly for domestic parts

By onBusiness Practices | Education | Insurance | Market Trends | Repair Operations

Editor’s note: Mitchell has allowed us to reproduce (with minor RDN stylistic edits) this feature story from its free second-quarter Industry Trends Report released today. In it, analyst Nate Raskin shows just how aggressively OEMs have slashed prices to compete with aftermarket components. Those who find the piece valuable shouldn’t miss the rest of the Industry Trends Report for other data a collision repairer can use to make informed business decisions.

By Nate Raskin

The last time I saw the Big Deal was back in 2010. The 6’5”, 520-pound intimidator was hard to miss, strong-arming deals as William Shatner’s sidekick for Priceline.com. When Priceline pitched Shatner off a cliff during a 2012 Super Bowl commercial, it signaled an end for the Big Deal. Admittedly, I was bummed. I always liked the Big Deal – he was a savings machine, he had matching “Dollars” and “Sense” tattoos, and he wore a white fur coat. Now that’s what I call a trifecta.

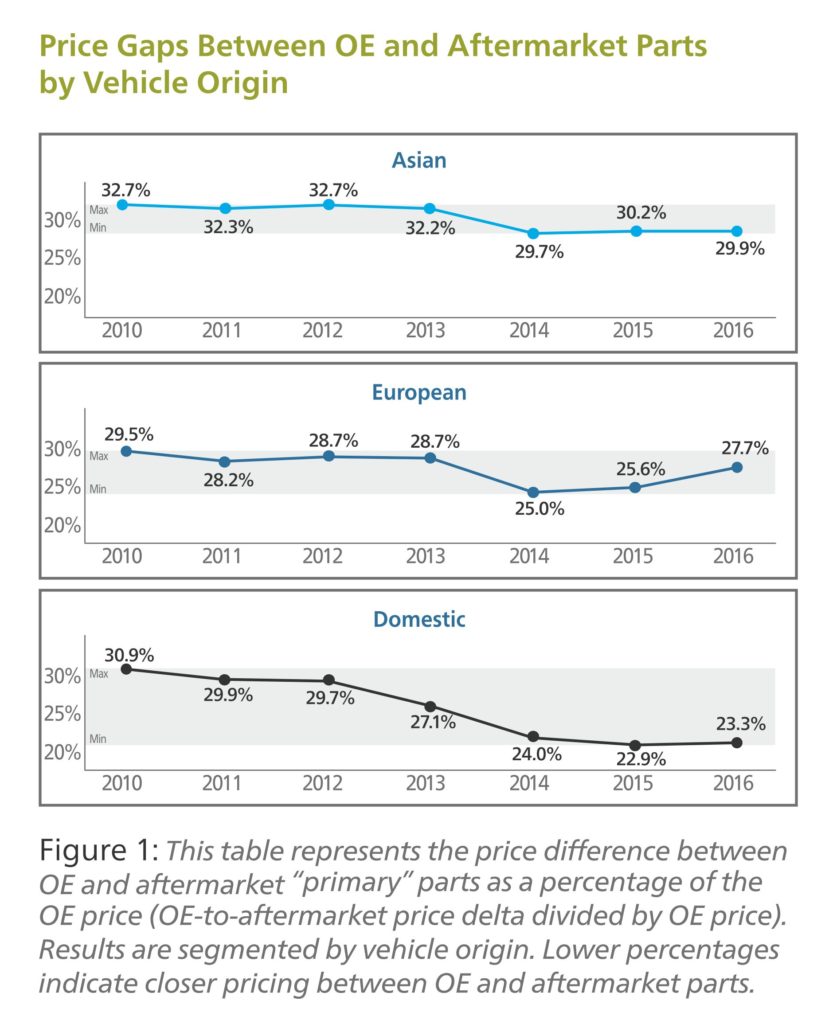

For insurers and price-conscious consumers, aftermarket parts have long played the role of the Big Deal, representing the largest opportunity for collision repair cost savings. But is this still the case? To answer this question, we analyzed millions of Mitchell estimate rows dating back to 2010, comparing OE and aftermarket part prices for six “primary” collision components (bumper covers, fenders, hoods, headlamps, rear combination lamps, and radiators).

For this analysis, we focused our attention on the average deltas, or price gaps, between OE and aftermarket primary parts. As our goal is to simply demonstrate trends, we grouped results to include both cars and trucks across all vintages, then segmented results by vehicle origin.

For example, our data suggest the average OE-to-aftermarket price gap for Asian makes shrank by 3 percent between 2010 and 2016. European makes followed a similar trend, as the average OE-to-aftermarket price gap closed by almost 2 percent over the same period. Translation – for Asian and European makes, aftermarket parts offer slightly less savings potential today (compared to OE) than they did seven years ago.

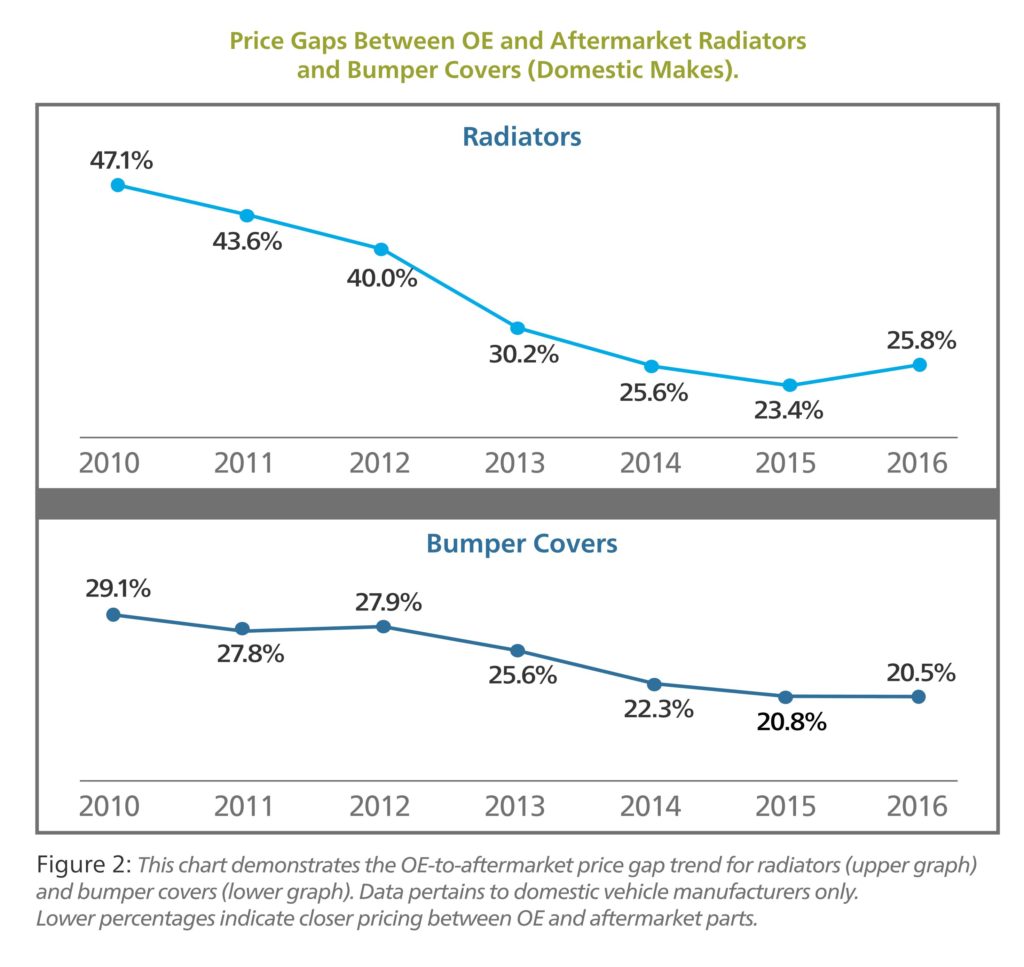

The domestic vehicle segment tells a more dramatic story. From 2010 to 2016, the average price difference between OE and aftermarket primary parts shrank by almost 8 percent. As it turns out, the reason we’re seeing a closing of the OE-to-aftermarket price gap with domestic vehicles has less to do with aftermarket increases and more to do with OE adjustments. Nothing exemplifies this trend more than radiators and bumper covers.

From 2010 to 2016, domestic OE radiator prices decreased by 26 percent, while domestic aftermarket radiator prices increased by 2 percent. Moreover, the average OE-to-aftermarket price gap closed by a whopping 22 percent over that span.

Bumper covers experienced similar movement, although not as extreme – domestic OE prices decreased by 2 percent, while aftermarket prices increased by almost 11 percent. From 2010 to 2016, the gap between OE and aftermarket bumper cover prices narrowed by 9 percent. The takeaway – for domestic makes, aftermarket parts savings are not as compelling as they were seven years ago.

Domestic OE price reductions on radiators and bumper covers is striking, because it’s not common to see part prices go down like that in our industry. What seems evident is that domestic OEs are paying close attention to aftermarket pricing and making adjustments to regain share. With greater access to data and the advent of dynamic pricing mechanisms, I anticipate we’ll continue to see OEs leverage technology to reach a competitive equilibrium.

In the end, there are plenty of factors that go into parts selection that extend beyond cost. If you’re simply looking to gauge OE versus aftermarket cost savings, it’s all about the price delta. For domestic makes, the shrinking OE-to-aftermarket price gap suggests manufacturers are reducing prices in a play to gain parts share. Such are the effects of competition. And while aftermarket parts may not quite be the Big Deal they were seven years ago, the big guy is still alive and kicking. He’s just working a few different angles.

Nate Raskin, Mitchell senior manager for APD Analytics, has over 17 years of experience in the auto physical damage sector. Raskin began his career in claims, learning the ropes as an estimator and team leader with Progressive before serving as the National Property Damage Manager at Unitrin Direct Insurance. Prior to his current role leading the Mitchell analytics team, he was a senior business consultant in Mitchell’s APD division, performing workflow visioning, SaaS solution design, and ad-hoc efficiency studies for partner carriers across North America.

Nate Raskin, Mitchell senior manager for APD Analytics, has over 17 years of experience in the auto physical damage sector. Raskin began his career in claims, learning the ropes as an estimator and team leader with Progressive before serving as the National Property Damage Manager at Unitrin Direct Insurance. Prior to his current role leading the Mitchell analytics team, he was a senior business consultant in Mitchell’s APD division, performing workflow visioning, SaaS solution design, and ad-hoc efficiency studies for partner carriers across North America.

More information:

“OE Versus Aftermarket Part Price Deltas: In Search of the Big Deal”

Nate Raskin in second-quarter 2017 Mitchell Industry Trends Report, June 13, 2017

“Mitchell Issues Second Quarter 2017 Industry Trends Report”

Mitchell, June 13, 2017

Mitchell Industry Trends Reports

Images:

General Motors’ MyPriceLink display at NACE on July 24, 2015. (John Huetter/Repairer Driven News)

Mitchell in 2017 compared prices for certain OEM and aftermarket parts from 2010 to 2016. (Provided by Mitchell)

Nate Raskin, Mitchell senior manager for APD Analytics. (Provided by Mitchell)