Calif. Dept. of Insurance: Insurers can’t have ‘Opt-OE’ parts on estimates either

By onAnnouncements | Associations | Business Practices | Insurance | Legal

Following a California BAR regulation clarifying that nebulous parts classifications like “Opt-OE” shouldn’t appear on repairer estimates, the California Department of Insurance confirmed Monday that there’s no place for them on insurer estimates either.

It would be an unfair claims settlement practice, CDI general counsel and Deputy Commissioner Kenneth Schnoll wrote to the California Autobody Assocation, which had sought a legal opinion on the behavior.

“You informed us that certain insurers use non-standard replacement crash part terminology and descriptions such as ‘Alt-OEM’, ‘Opt-OEM’, and ‘Surplus-OEM’ or other similar terms on their claims settlement estimates and appraisals,” Schnoll wrote. “You also informed us that these replacement crash parts may be over-production OEM parts, blemished or damaged OEM parts and that such parts may not carry the same new OEM part warranty. Additionally, we understand that different categories of crash parts are frequently combined by insurers on repair appraisals and estimates and called ‘Opt-OEM’, ‘Alt—OEM’ and other similar variations. For example, you informed us that various insurers list parts from an auto-dismantling vendor as ‘Used’ when those parts are actually new OEM parts.” (Minor formatting edits.)

Under the California Code of Regulations, collision repairers must give customers a estimated price for parts and labor that itemized each component, and each part “must be new unless specifically identified as a used, rebuilt, or reconditioned part,” Schnoll wrote.

Schnoll referenced the California Bureau of Automotive Repair’s recent rewrite of the California Code of Regulations to eliminate terms like “OPT-OEM” or “ALT-OEM.” (See our series for more on the topic.)

“As you can see, The BAR concern is that alt/opt OEM crash parts lack a specific definition and could be misleading,” California Autobody Association lobbyist Jack Molodanof (Molodanof Government Partners) wrote in a September email. “What exactly is an alt/opt OEM crash part ? Some definitions simply lump together several possibilities of what the part maybe (e.g blemished, slightly damaged, etc) In other cases these parts may not carry the original OEM warranty. In other cases, these parts may not even be OEM. Therefore using terms like opt/alt OEM without a specific and clear definition may be considered misleading and subject the shop to disciplinary action.”

Opt-OE parts are a concern because aside from a few formal programs by automakers themselves — selling parts which may or may not be warrantied — there’s no way for the customer to know what they’re buying. It seems to be whatever the vendor wants to declare “Opt-OE.” The part might be new, and acquired and resold at a discounted price. It might be new, but from another part of the world. The vendor might in good faith think they’re new — only to find out they’re counterfeits.

Schnoll also mentioned that body shops are bound by the California Business & Professions Code, writing that it “requires that each written estimate of the cost of the auto body or collision repairs indicate whether each crash part is either an OEM part or a non-original OEM aftermarket crash part and whether each replacement part is new, used, rebuilt, or reconditioned.”

“No other description of replacement crash parts is permissible under the Business & Professions Code,” he continued. “Accordingly, because no other name or designation for replacement parts is permissible under the Business & Professions Code, the use of any terms other than original OEM or non-original OEM in a repair estimate, such as ‘Optional OEM,’ ‘Alternate OEM,’ or ‘Surplus OEM’ is not permitted.”

In a situation where a body shop wrote an estimate on behalf of the insurer, it still counted as an estimate from an auto body shop — which meant the shop was still bound by the Business and Professions Code and California Code of Regulations, according to Schnoll. The shop working on behalf of the insurer still had to classify parts one of four ways — new, used, reconditioned or rebuilt — and say whether crash parts were OEM or aftermarket.

“Accordingly, because insurers are required to follow the same standards as auto body collision repair shops in connection with repair estimates, insurers are also prohibited from using any description of any replacement part other than new, used, reconditioned, rebuilt, an OEM crash part, or a non~OEM aftermarket crash part,” Schnoll wrote.

The California Code of Regulations states that any estimate used to settle a loss written “by or for the insurer shall be of an amount that will allow for repairs to be made in accordance with accepted trade standards for good and workmanlike automotive repairs by an ‘auto body repair shop’ as defined in section 9889.51 of the Business and Professions Code, and in accordance with the standards of automotive repair required of auto body repair shops as described in the Business and Professions Code and associated regulations, including, but not limited to, Section 3365 of Title 16 of the California Code of Regulations. An insurer shall not prepare an estimate that deviates from the standards, costs, and/or guidelines provided by the third-party automobile collision repair estimating software used by the insurer to prepare the estimate, if such deviation would result in an estimate that would not allow for repairs to be made in accordance with accepted trade standards for good and workmanlike automotive repairs by an auto body repair shop, as described in this subdivision.”

Schnoll also pointed out that insurers were bound by the California Insurance Code not to say anything “which is untrue, deceptive, or misleading, and which is known, or which by the exercise of reasonable care should be known, to be untrue, deceptive, or misleading.” Using terms like “Opt-OE” were at best misleading and at worst deceptive, he suggested.

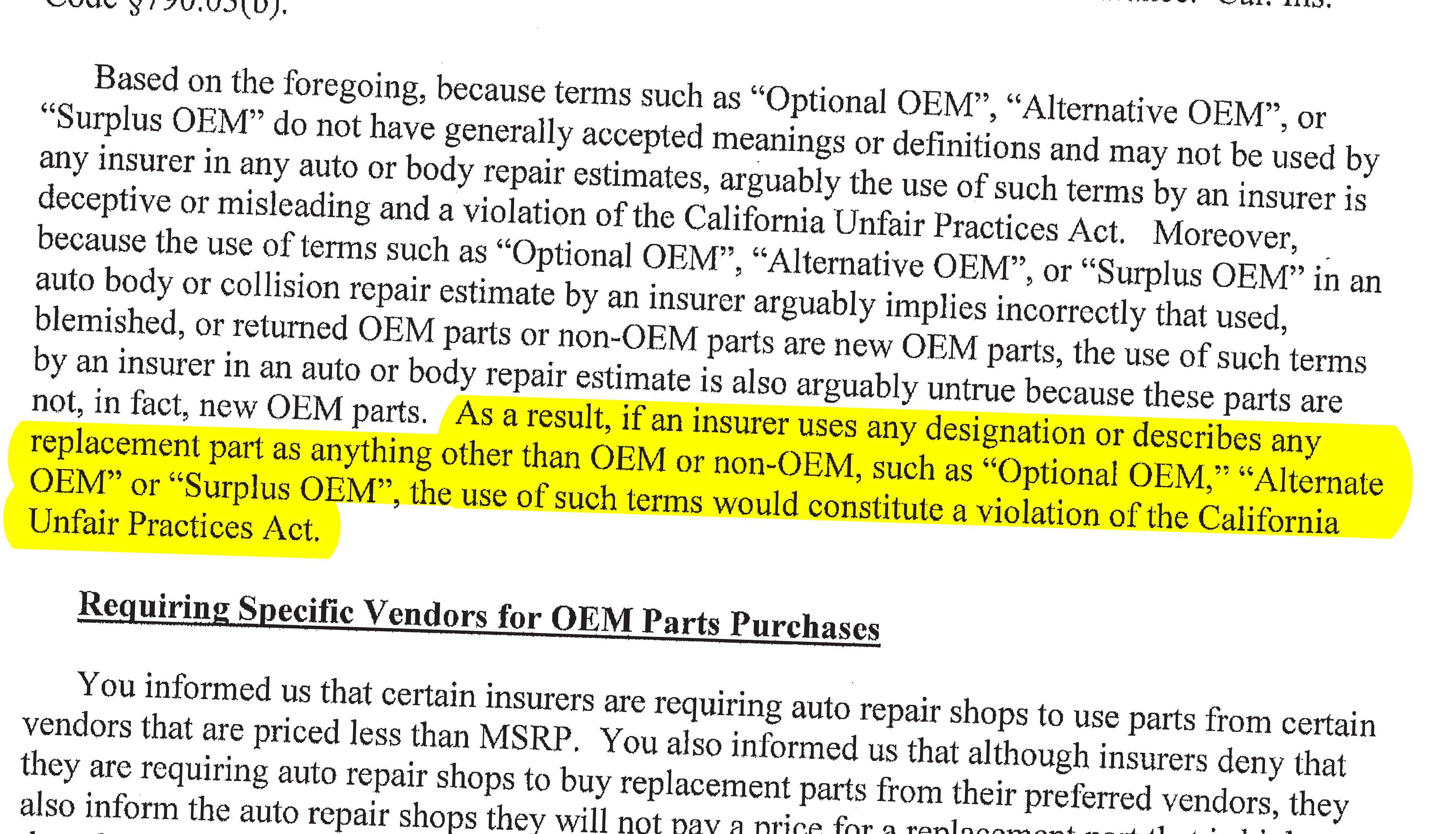

“Based on the foregoing, because terms such as ‘Optional OEM’, ‘Alternative OEM’, or ‘Surplus OEM’ do not have generally accepted meanings or definitions and may not be used by any insurer in any auto or body repair estimates, arguably the use of such terms by an insurer is deceptive or misleading and a violation of the California Unfair Practices Act,” Schnoll wrote. “Moreover, because the use of terms such as ‘Optional OEM’, ‘Alternative OEM’, or “Surplus OEM’ in an auto body or collision repair estimate by an insurer arguably implies incorrectly that used, blemished, or returned OEM parts or non-OEM parts are new OEM parts, the use of such terms by an insurer in an auto or body repair estimate is also arguably untrue because these parts are not, in fact, new OEM parts. As a result, if an insurer uses any designation or describes any replacement part as anything other than OEM or non-OEM, such as ‘Optional OEM,’ ‘Alternate OEM’ or ‘Surplus OEM’, the use of such terms would constitute a violation of the California Unfair Practices Act.” (Minor formatting edit.)

California shops interested in hearing more from the Bureau of Automotive Repair about collision repair should attend a public workshop Oct. 18, scheduled for 2 p.m., after its advisory board meeting at 9 a.m.

“The workshop will be focused on the collision repair industry,” Ramos wrote in an email Tuesday. “We will hear feedback from stakeholders on possible regulation updating.”

Images:

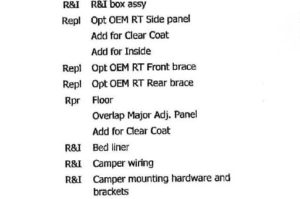

An estimate contains references to Opt-OE parts. (Provided to Repairer Driven News)

Following a California BAR regulation clarifying that nebulous parts classifications like “Opt-OE” shouldn’t appear on repairer estimates, the California Department of Insurance confirmed Oct. 8, 2018, to the California Autobody Association that there’s no place for them on insurer estimates either. (California Department of Insurance letter; Provided by California Autobody Association)

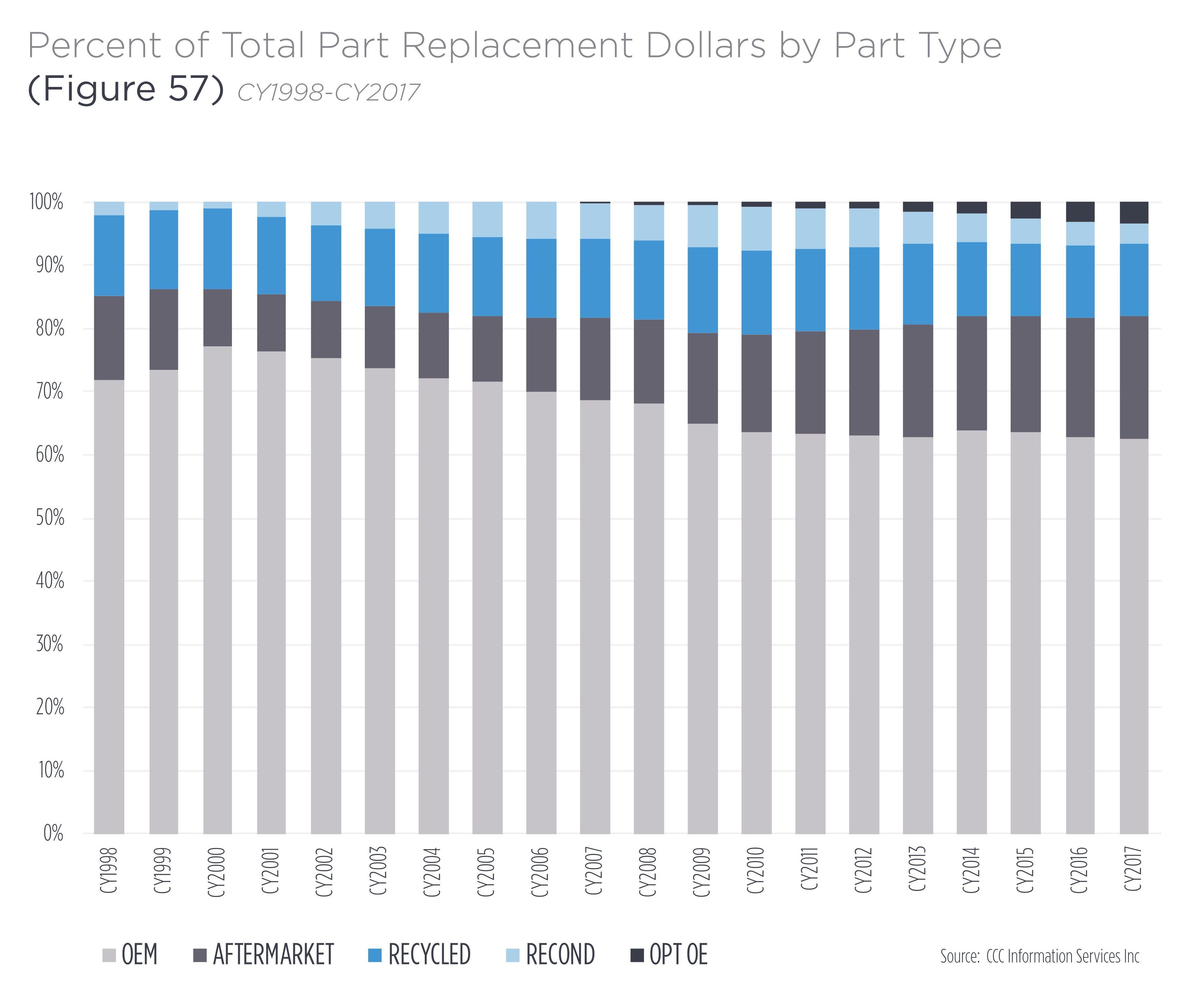

The proportion of parts spend allocated to each part type on CCC estimates is shown on data from CCC’s most recent “Crash Course.” (Provided by CCC)