Record 401(k) lawsuits focus attention on employers’ fiduciary responsibility

By onAssociations | Business Practices | Market Trends

A record number of lawsuits were filed over costly and poorly performing 401(k) plans in 2020, with numbers continuing to rise in 2021. At the same time, employment market forces and state legislation are leading more and more employers to consider offering retirement savings plans to their employees.

For these reasons, shop owners who offer 401(k) plans might want to consider reducing their fiduciary risk through the SCRS Multiple Employer Plan, which puts plan oversight into diligent hands.

In a July 25, 2021 article in Forbes magazine, contributor Brian Menickella, co-founder of The Beacon Group of Companies, said that most of the 401(k) lawsuits are tied to “Hefty fees, expensive options with low returns, limited investment options, and draconian terms” associated with the plans. Experts attribute the trend to two major factors: the increasing availability of data analyzing the performance of 401(k) plans; and the pandemic, which has led employees to more closely examine their retirement plans.

According to a Sept. 8, 2021 article in Bloomberg Law, 401(k) lawsuits have garnered more than $430 million in settlements in recent years. Among those settling have been some big names, BlackRock Institutional Trust Co., Reliance Trust Co., McKinsey & Co., SunTrust Banks Inc., Fidelity Investments, BB&T Corp. and Deutche Bank among them.

Current risk landscape

Scott Broaddus, the investment adviser for the SCRS association 401(k) program, spoke with RDN about the current fiduciary risk landscape, and how the SCRS Multiple Employer Plan helps to offset shops’ risk exposure.

Broaddus said the wave of lawsuits over poorly-performing 401(k) plans began about eight or nine years ago, mostly with Fortune 500 companies related to excessive costs and conflicts of interest. He likened the cost factor to small businesses buying a can of soda at a convenience store, versus the SCRS coming together to buy the same soda at Costco, where bulk buying results in a lower unit price.

Many businesses underestimate the time that goes into administering a retirement plan, and fail to recognize the ramifications if the plan is not administered correctly, he said.

“An employer sponsored plan starts with designing a benefit that will best meet your needs,” Broaddus said. “When will an employee become eligible, are Roth contributions permitted, is there a matching program. Testing is required annually by the Department of Labor along with annual notices. We find that the employee tasked with HR in many small businesses is also responsible for other duties as well. Having a partner to help navigate this important benefit has been beneficial for members participating in the SCRS plan.”

80% increase in lawsuits

Menickella, in the Forbes article, stressed the importance of understanding the basis for the rising tide of lawsuits, and what to look for in a plan to make certain that the employers’ fiduciary responsibility to their employees is met.

“The number of Employee Retirement Income Security Act (ERISA) lawsuits in 2020 doubled the number of ERISA lawsuits in 2018 and had an 80% increase from 2019,” Menickella said. “Last month, CDI Corp. in Philadelphia was ordered to pay $1.8 million to settle a class-action lawsuit that claimed there was no system to evaluate its 401(k) plan’s investment options, leading to plans only offering actively managed, expensive funds. This settlement benefited more than 4,000 people covered by the $247 million retirement plan.

“CDI Corp joins a growing list of firms facing proposed class actions lawsuits by retirement plan participants decrying the exorbitant fees. Several employers, such as Cerner Corp. and Quest Diagnostics DGX +1%, have been sued multiple times over plans being too expensive, and companies like Russell Investment Management LLC continue to be sued over poor-performing 401(k) plans.”

“The rate of companies settling 401(k) lawsuits indicates that companies have been enrolling their workers on flawed retirement plans,” Menickella concluded. “With these facts in mind, you should evaluate your employer-provided 401(k) on four merits: expense ratio, restrictions, investment options, and investor education. Addressing these factors can help you pick a retirement plan that enables you to build a generous nest egg for your golden years.”

Costs not always obvious

Complicating matters, Broaddus said, is the fact that the total costs of a plan are not always immediately obvious to a company owner or CFO.

He said owners will frequently tell him, “‘My plan is very inexpensive, I get an invoice each year for $800. Saving me 20% of $800 is not worth the time and the energy to make that switch.’ What they don’t realize is the invoice that they receive may only make up 5% of the total cost of the plan. Often, plan expenses are charged against participant account balances. If a participant is helping pay 95% of administrative expenses, it’s understandable to see how a lawsuit may originate if expenses are excessive.”

“It is the responsibility of the owner of the company, or anyone who’s helping in administration of that 401(k) plan, to act in the best interests of the participants of that plan. And that means that as your plan grows, you need to be comparing your costs to what is available in the marketplace,” he said. “Many vendors charge as a percentage of plan assets, so if your plan balance has risen 40% with the stock market in the past year, so may have your expenses.”

An employee’s dissatisfaction does not have to result in a lawsuit to be problematic for a business owner, Broaddus added. “Sometimes an employee came from a very large place, that had a very professional looking retirement plan. And they’re now starting to ask questions if revenue sharing is being credited back to the plan, or why only one fund family is represented. At that point you’re playing defense; getting out in front and proactively addressing these issues is smart risk management.”

Broaddus offered his appreciation for the work of the Investment Committee of the SCRS Board, which oversees the SCRS MEP program.

“I work with nonprofits and associations all across the country who manage retirement plans for employees and their members. “Before deciding to offer a retirement solution to their members, SCRS spent 18 months learning about everything from plan designs, to vendors and options that already exist. They ultimately picked a plan that was tailor-made for their membership, hired the vendors and negotiated pricing up-front that declines for all participants as the plan grows. SCRS Executive Director Aaron Schulenberg and the Investment Committee have been amazing advocates for the participants in this plan.” He concluded, If a decision needs to be made, the first question the SCRS Investment Committee asks is, ‘Is this in the best interest of our members and their employees?’. I wish more plan sponsors started with this simple question.”

When employees sue

What are the primary drivers behind the lawsuits? According to a Feb. 2, 2021 article in the National Law Review by Howard Shapiro, René E. Thorne and Lindsey H. Chopin of Jackson Lewis P.C. Publications, they include:

- Excessive administrative fees (based on use of more than one recordkeeper; absence of competitive bidding; use of asset-based fees and revenue-sharing instead of, or in addition to fixed-dollar fees; failure to monitor fee payments to recordkeepers; and/or, occasionally, kickbacks);

- Excessive management fees and performance losses (duplicative investment options for each asset class, which underperformed and charged higher fees than lower-cost share classes of certain investments);

- A failure to monitor and evaluate appointees.

Complainants also allege that:

- The funds charge excessive fees;

- The funds are imprudent investment options because, net of fees, they offer inferior performance to available alternatives; and

- The payment of fees to an affiliate constitutes a prohibited transaction. In 2020, the outcome in fee cases was mixed.

Menickella advises that “The ideal retirement plan carries a diverse range of investment options, including low-cost stock funds, low-cost target-date funds, and several bond index funds. Some plans may include ‘actively managed’ funds where a portfolio manager actively manages or trades the positions but frequently cannot match the performance of their correlated index. Be wary of a 401(k) plan with no low-cost funds because they might prove expensive in the long term.”

One important way to evaluate a retirement plan, Menickella said, is by the fee structure, and particularly the expense ratio.

“The ideal expense ratio is 0.20% or less, while anything above 1% is indefensible and usually is representative of “revenue sharing”. Revenue sharing is defined as a deliberate overcharge at the expense ratio level used to pay the vendors of the plan such as a third-party administrator, recordkeepers, brokers, or financial advisors. These hidden overcharges come in the form of eroded returns and have been at the heart of a great deal of these 401k lawsuits. These fees are difficult to uncover and are typically buried deep within the Service Provider 401k Fee Disclosure Document, form 408(b)2“, he said.

“A 401(k) plan with a total ‘all-in’ fee, where total costs are expressed as a percentage of assets in the plan, between 0.50% to 1% is typically okay, depending on the size of the plan. The Department of Labor requires employers to monitor these fees and failure to do so is considered a fiduciary breach that can result in stiff fines and penalties. High expense ratios with revenue sharing fees built-in can lead to a significant negative impact on an individual’s bottom line over the lifetime of the investment.”

The Department of Labor offers a 401(k) Plan Fees Disclosure Tool, which it describes as “a form developed by banking, insurance and mutual fund trade groups to provide employers with a way to collect and compare investment fees and administrative costs of competing providers of plan services.”

A push for savings plans

Employers have long recognized the value that offering retirement benefits, such as 401(k) plans, have in attracting and retaining employees. Now, a growing number of states are beginning to mandate retirement savings plans for private sector workers.

“Businesses offer retirement plans for different reasons: Some may use the match as a form of employee profit sharing, others feel it’s necessary to recruit the best talent,” Broaddus said. “But now some states are getting involved and passing legislation that will require companies to offer a retirement plan. With 25% of the workforce looking to retire in the next 10 years I expect this will be a major focal point for states.”

“Partially due to the belief that there exist significant gaps in access to retirement savings plans as what is keeping Americans from savings, many states have considered legislation that would implement state-run IRA-type retirement plans,” the National Association of Insurance and Financial Advisors said on its website. “Under these proposals, employers who do not already offer their employees a work-based retirement plan would be required to participate in the state-run program. Their employees would be automatically enrolled in the state-run plan but would be able to opt- out of participating in the program.”

So far, NAIFA said, “Nearly 40 states have considered legislation that would establish a state-run retirement plan. To date, California, Connecticut, Colorado, Illinois, Maryland, New Jersey, Oregon and Virginia are the only states that have enacted legislation establishing a state-run plan program. Due to numerous legal and cost concerns, only three of these state plans have been implemented or become operational (CA, OR and IL). These programs are flagging with high employee opt-out rates, low contributions, high employee turnover, and high account withdrawal rates. No other state has enacted legislation establishing a state-run retirement plan. Washington State and New Jersey have enacted legislation which sets up voluntary retirement marketplaces designed to bring together employers and private market plan providers.”

Images

Featured image: Document with title 401k plan on a table. (designer491/iStockphoto)

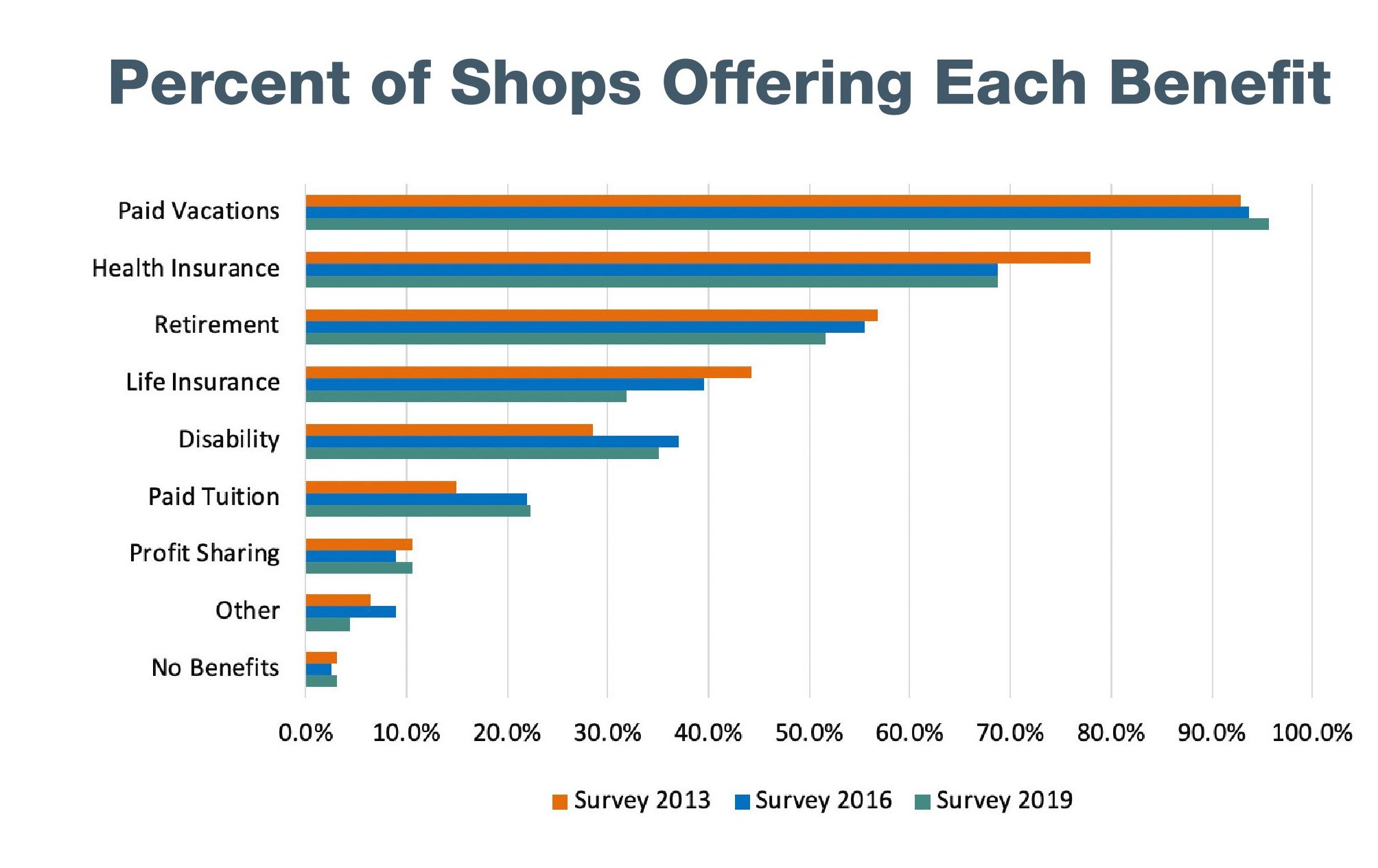

A smaller percentage of shops reported offering life insurance and retirement in 2019 than in 2016, according to a Collision Repair Education Foundation and I-CAR study that polled more than 675 shops. (Provided by CREF)

More information:

Why SCRS members have better 401(k) options

Recent uptick in 401(k) lawsuits highlights fiduciary risk to employers

Considering offering, switching a 401(k) at your body shop? Check out SCRS webinars