Auto insurers told to disclose pandemic profits in Illinois

By onInsurance | Legal

The Illinois Department of Insurance has directed auto insurers to disclose detailed information about the profits they made during 12 months of the COVID-19 pandemic lockdown.

The request, issued Wednesday, follows a letter sent by 16 state senators and nine advocacy organizations in January urging the department to act. Insurers were given until May 15 to respond, with the information to be made public on the department’s website by June 30.

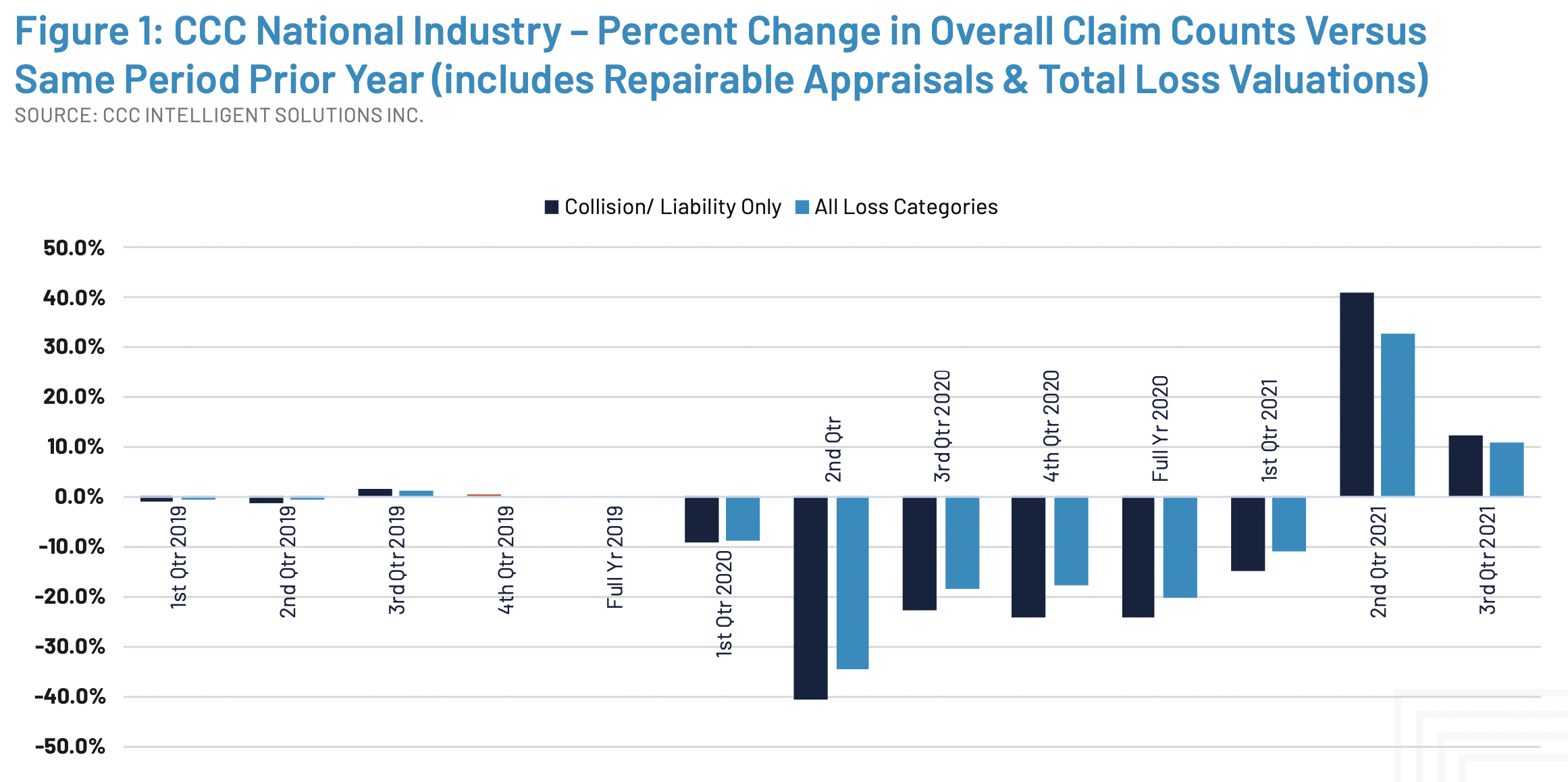

Consumer groups analyzing insurers’ underwriting performance from 2020 have concluded that auto insurers reaped billions of dollars in excess profits due to reduced accidents during the pandemic lockdowns, and say consumers are still owed billions in additional refunds.

“Insurers selling personal auto insurance reaped windfall profits of at least $29 billion in 2020 as miles driven, vehicle crashes and auto insurance claims dropped because of the pandemic and related government actions,” according to the Consumer Federation of America (CFA) and Center for Economic Justice (CEJ).

The groups’ analysis shows that insurers collected $42 billion in excess premiums while refunding only $13 billion in “premium relief” payments to consumers.

The California, New Mexico and Washington insurance departments have issued similar data calls to more fully assess how mileage reductions affected insurers’ exposure to risk or loss.

Though many insurance companies have issued some refunds in response to public pressure, CFA has estimated that they could still owe Illinois car insurance customers $896 million in relief.

“We applaud the Department of Insurance and Pritzker administration for today’s action,” Illinois PIRG Education Fund Director Abe Scarr said in a statement. “If the data show, as we expect, that insurers made windfall profits during the pandemic, we’ll call on them to issue additional customer refunds.”

Illinois state Sen. Jacqueline Collins issued a statement cheering the move, but also noted that more must be done to protect consumers.

“As chief sponsor and primary advocate for a number of consumer protection measures, it has long been my mission to prevent predatory business practices impacting the hardworking and historically disadvantaged individuals within our communities,” Collins said. “The Illinois Department of Insurance has shown its commitment to bettering our financial systems and defending the wellbeing of policyholders, and for that I am grateful. However, there is still much work that needs to be done if we are to effectively and successfully preserve public interests.”

Michael DeLong, a research and advocacy associate with CFA, sounded similar themes.

“This data call is a good first step, although much work remains to be done,” said DeLong said in a statement. “Insurers raked in massive profits during the pandemic, while many consumers were struggling to make ends meet. And they only gave back limited amounts, using the rest of those profits to enrich their shareholders and CEOs.”

What authority the Department of Insurance might have to respond to windfall profits is not clear. Illinois is one of only two states whose auto insurance regulators have no power to reject or modify rate hikes, according to Illinois PIRG. Illinois law also does not prohibit “excessive” rates like most states do.

“Illinois has among the weakest auto insurance rate consumer protections in the country, so we appreciate regulators exercising the authority they do have,” Scarr, director of the public interest research group, said. “We look forward to working with the Department and Illinois policymakers to improve auto insurance consumer protections going forward.”

Labeled “Market Conduct – Market Analysis,” the one-page letter asks insurers to provide nine specific pieces of data for the 12-month period between March 2020 to February 2021, when many people had significantly reduced their driving.

The categories listed in the letter are:

- Earned Vehicle Exposures

- All expenses other than loss adjustment expenses, excluding amounts from item 5 below

- Net Earned Premium Before Application of any COVID-19 related Premium Credit/Refund/Dividend

- The Amount of any COVID-19 related Premium Credit/Refund/Dividend accounted for as premium

- The Amount of any COVID-19 related Credit/Refund/Dividend accounted for as expense

- Net Ultimate Incurred Losses and Defense and Cost Containment Expenses

- Net Ultimate Adjusting & Other

- Ultimate Reported Claim Counts (Excluding Claims Closed without Payment)

- Open Claim Counts

The department said that all information, with the exception of “earned vehicle exposures,” would be considered non-proprietary, and made public. Earned vehicle exposures will be made public in the form of a weighted average frequency across all companies.

More information

Auto insurers scored windfall profits from pandemic lockdowns

Ruling casts doubt on Calif.’s ability to order $3.5B in auto insurance premium refunds

Images

Featured image provided by sefa ozel/iStock